Stay up up to now with free updates

Simply register for Artificial intelligence myFT Digest – delivered straight to your inbox.

Goldman Sachs desires to make it clear that it’s anti-gene AI. Some of you could have misunderstood the matter after the bank published a report in June titled “Generation AI: Too much spending, too little profit?” – but notice the query mark! You are only asking questions!

Goldman strategist Peter Oppenheimer and his team released a follow-up this morning that seeks a deeper understanding of what they call the “rational exuberance of technology.” Here's the summary:

The technology sector has generated 32% of worldwide equity returns and 40% of the U.S. equity market return since 2010. This is resulting from stronger fundamentals slightly than irrational exuberance. Globally, the technology sector has seen earnings per share rise by about 400%, while all other sectors combined have gained about 25% from their pre-global financial crisis peak.

So it's not a bubble. But there are limitations.

The problem with any good story is that it “can increase interest to the purpose where it monopolizes investor attention on the expense of other opportunities. This can result in unrealistic expectations about future earnings and make firms vulnerable to a big downgrade,” say Oppenheimer et al.

Disruptive technologies almost at all times undergo a boom-bust-boom, with big players doing useful things only emerging once the initial bubble bursts under the burden of opportunistic me-too firms. The same risks and opportunities emerge in each cycle, says Goldman:

In the past, investors have focused an excessive amount of on the inventors, underestimated the influence of competition and overestimated the returns on capital of early innovators. At the identical time, investors are inclined to underestimate the expansion of latest entrants who can profit from the investments of others and thus develop recent services. Valuation also often underestimates the opportunities that may arise in non-technology industries that may use technology to generate higher returns in existing and recent product categories.

The survivors drive their plows over the bones of the dead, says Goldman, but puts it this manner: “The infrastructure that’s left behind within the wake of the initial wave of investors and capital spending results in the creation of latest services.”

AI isn’t exactly like previous innovation bubbles (books, channels, radio, telegram, radio, etc.) because many of the dominant firms were the winners of the previous bubble, Goldman continues. Raising money from promoting means they will burn through their capital expenditures – but even current spending rates won't give them insurmountable monopolies on whatever comes out of it, the team argues:

Although the present AI winners are surrounded by a powerful protective wall and valuations aren’t bubble-like, the number of latest patents in the sphere is growing rapidly, suggesting that recent competitors will emerge and costs will fall. (…) While the hyperscalers have enormous capability and the flexibility to speculate in proprietary AI models, cheaper open-source alternatives are emerging at a really fast pace. The website Hugging Face, a network for enthusiasts, already has around 650,000 models, suggesting that the everyday pattern of capital growth and competition on a big scale is playing out within the AI field, just as in previous technology waves.

Just as competition is usually underestimated, returns on investment spending on innovation are also typically overestimated because the marginal cost of technology declines and capability increases over time, Goldman adds:

With most major technological innovations in history, while the potential is apparent, it isn’t clear within the early stages which business models will ultimately prevail to scale and commercialize the technology. This was clearly evident within the early days of the Internet. While there was widespread and broad-based speculation about every recent company that promised potential exposure to the industry, the established winners were generally the telecommunications firms. They were seen as a comparatively “protected” path to the potential fortunes the Internet could generate in comparison with the more speculative, unprofitable dot-com firms. ( . . . )

As with other examples throughout history, the issue was not a miscalculation of the technology's growth potential, but slightly that investors had assigned an excessive amount of future value to the businesses that had developed the technology and infrastructure to deliver it. In this case, as in lots of others before it, the final word winners were the businesses that might “freely profit” from this expenditure and use the capability to develop business models that might leverage the technology and offer recent services. Many of those winners only emerged with the introduction of the smartphone in 2006 and the launch of apps, which then spawned a growing industry of platform firms, ride-sharing services, social media, and so forth.

To reiterate: no bubble (in comparison with previous bubbles that were definitely bubbles):

Still, “today's AI winners are not any longer capital-poor firms,” says Goldman. “Just as we saw with the web's networking firms, AI is driving a large investment boom and threatening to stifle the high returns which have characterised the sector for the past 15 years and that, at current valuations, will proceed.”

And there’s little evidence that technological investments extend the lifetime of mental property or that pioneers like ChatGPT have the endurance needed for industrial success:

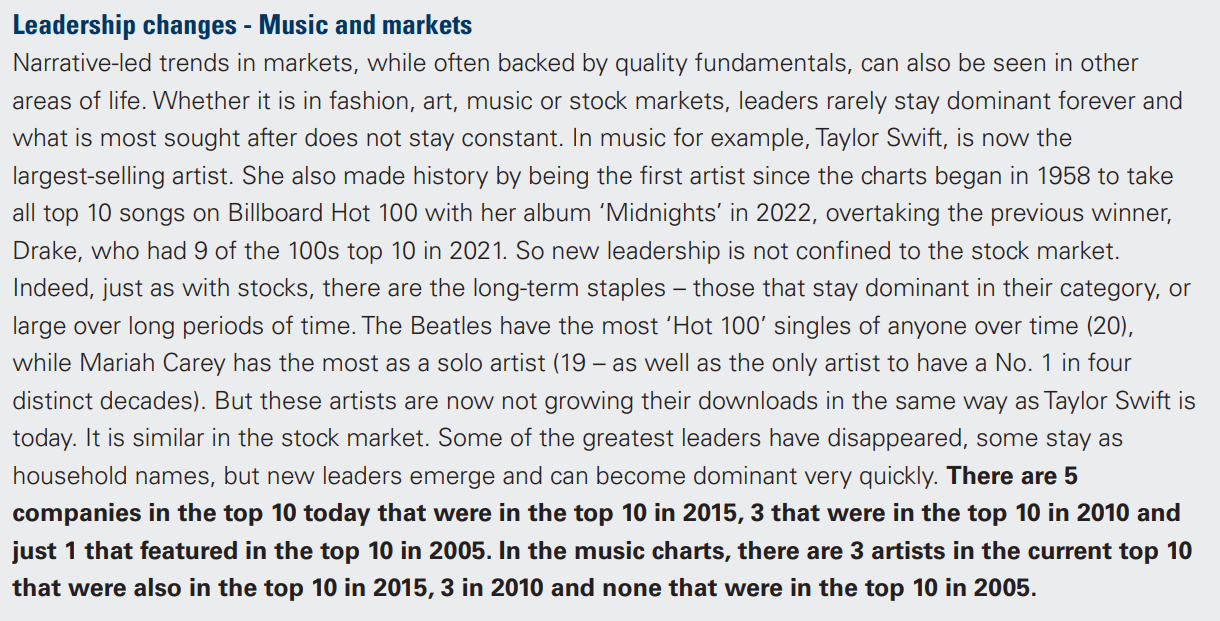

Oppenheimer and his team provide an introduction to concentration risk and the regularity with which market leadership changes. We won't repeat this as it’s going to be familiar territory for normal readers. If you would like to read Goldman's section on the longevity of pop music artists and stock market winners, there’s a screenshot here.

There can also be speak about how technology is inherently deflationary, which might be good for avoiding antitrust scrutiny, but not so good for defending margins:

So, to sum up, investors should diversify. Instead of shopping for more Nvidia, a greater option to play the Gen-AI theme could be to… buy.

LVMH?

Because of Bake Off?

In previous technology cycles, the second-round impact on work and society has often driven recent areas of consumption growth. For example, more AI is more likely to mean greater demand for fact-checking services. The ability to work more productively from home may mean a revival of shopping and entertainment in high-density neighborhoods. The growth of artificial immersive entertainment may drive demand for real-world experiences. This could reflect the growing popularity of products and services seen as “authentic” or nostalgic. Retro “crafts” are growing in popularity, whether within the growing reality TV shows that pit contestants against one another in baking, spelling, sewing, and even ballroom dancing competitions. ( . . . )

In the twenty first century, in a highly digitalised world where almost everyone seems to be connected to the web and cutting-edge technology threatens to displace jobs and businesses, it is critical that LVMH is one among the biggest firms in Europe. This is an organization that sells the worth of the heritage of historic brands. ( . . . )

As the ubiquity of technology increases and other people rely more on it to speak across networks, also they are more likely to value “authenticity” and human connection more highly – which can evoke nostalgic images of a less complicated, pre-digital life.

That's right, bitch.

For any second-wave AI company seeking to raise money in the present non-bubble (in addition to just about another company doing almost the rest), Goldman Sachs is on the market for all of your investment banking needs.

Further reading:

— The AI hype isn’t a repeat of the dotcom bubble, but a remix (FTAV)

{kind=link}

{kind=link}